Banking Deserts and Cash Availability

The number of bank branches in the U.S. has been declining for decades as a result of bank mergers, online banking, and banks looking for ways to reduce costs. This problem becomes even more pronounced after natural disasters when the demand for cash rises substantially and banks struggle to keep their branches and ATMs operating.

Natural disasters strike unexpectedly, and they’re happening more frequently and with greater intensity than ever before. According to the Centre for Research on the Epidemiology of Disasters (CRED), “disaster events have increased from 100 per year in the 1970s to around 400 events per year worldwide in the past 20 years.” With every new disaster, the economic impact increases as well.

As the prevalence of natural disasters continues to increase, banks face new challenges in maintaining cash availability and operational continuity in the aftermath of these storms.

The importance of cash during emergencies becomes clear when people flock to ATMs before and after a disaster strikes. This makes access to ATMs even more important and highlights the necessity of banks keeping up with the demand for cash by keeping their terminals operating and well supplied.

Banking Deserts in the U.S. Are on the Rise

A 2024 report by the Federal Reserve Bank of Atlanta indicated that 12 million people live in banking deserts today, and the rate of bank branch closures has doubled since 2020. The areas where banking deserts exist are:

- 66% suburban areas

- 20% urban areas

- 14% rural areas

What Are Banking Deserts?

The Federal Reserve reports that in 2024, 4% of census tracts in the United States were banking deserts and 4% could become a desert if just one branch closed. The Fed defines a banking desert that doesn’t have a bank branch within a certain radius from its population center, such as:

- 2 miles for urban communities

- 5 miles for suburban communities

- 10 miles for rural communities.

The Challenges of Banking Deserts

According to the Fed, having access to a bank is directly linked to residents having a higher percentage of mortgages, and at lower interest rates, than compared to areas without easy access to a bank.

A lack of banking services and limited access to cash in banking deserts can also lead to consumers using alternative financial sources, such as payday lenders, check-cashing services, and pawn shops which typically charge higher fees and interest rates. This increases the cost of banking services for residents and reduces their ability to save.

These problems tend to affect those with lower incomes, older adults, people living with disabilities, and rural consumers. A lack of bank branches also tends to coincide with a lack of broadband Internet connections. This makes it hard for people to bank online and difficult for people to obtain financial services in rural areas.

This is part of a long-term trend. A report by the National Community Reinvestment Coalition in 2022 indicated that two-thirds of banking institutions have disappeared, from 18,000 in 1984 to less than 5,000 in 2021. Mergers and acquisitions were behind many branch closures, along with a shift to mobile and Internet-based transactions.

How Disasters Affect Banks

Weather-related natural disasters in the United States significantly weaken the financial stability of banks in the affected regions, according to an analysis published in the May 2023 edition of the Journal of Environmental Economics and Management.

By analyzing more than 20 years of data, the study concluded that disasters increase the probability of loan defaults and foreclosures, lower returns on assets, and lower equity ratios of the affected banks in the years following a disaster.

The study also found that while insurance and public aid programs do help the affected areas, it’s not enough to offset the negative financial impact on the banking sector within a disaster area.

The Economic Cost of Natural Disasters

A lack of banking services becomes even more pronounced when national disasters strike, especially when electricity shuts down access to branches and ATMs. Internet and cell phone access can also be disrupted, which shuts down digital banking.

Events like hurricanes Helene and Milton, and the devastating fires in California and Hawaii, are part of a growing pattern of climate-driven disasters that include severe storms, floods, tornadoes, and tropical cyclones.

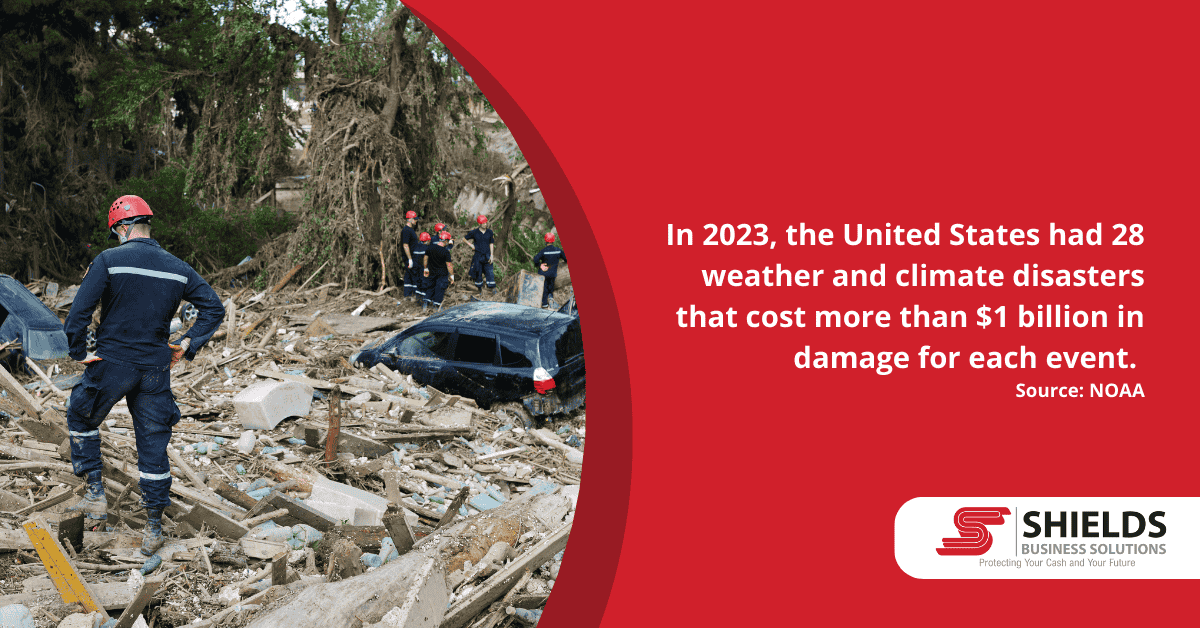

In 2023, the United States had 28 weather and climate disasters that cost more than $1 billion in damage for each event, according to the National Oceanic and Atmospheric Administration. Damage from all natural disasters in 2023 added up to $92.9 billion.

Banks and ATMs aren’t immune from such disasters that damage their facilities and cut off their supply of electricity and communications—at a time when their customers are often desperate for a supply of cash and other services.

After many disasters, cash is a vital commodity for the victims and aid organizations helping them, because it gives them the flexibility to buy whatever supplies they need, and their needs can change daily.

In the aftermath of Hurricane Helene in September 2024, Fed Chairman Jerome Powell said the Fed would work with banks in the affected areas to ensure they had enough cash available for their customers.

After disasters, the Fed works with banks to exchange damaged and contaminated cash. Its other efforts may include:

- Encouraging banks to waive ATM fees for customers and noncustomers.

- Increasing ATM daily cash withdrawal limits.

- Waiving overdraft fees.

- Easing restrictions on cashing out-of-state and non-customer checks.

- Increasing credit card limits for creditworthy customers.

- Waiving late fees for credit cards and other loan balances.

How to Keep the Cash Flowing

One of the ways that banks can deal with the cost of a natural disaster in their area is to outsource their ATM operations to reduce costs and improve operability.

As a leader in ATM solutions, Shields Business Solutions offers both ATM Service and Cash Replenishment, which is increasingly important given the increasing numbers of banking deserts and natural disasters.

More Efficient Cash Handling

We’re a leading provider of cash and ATM services in the NJ/PA/DE/NY area, and a provider of Branch Transformation services as well. With our Cash-In-Transit services, we reduce the burden of your cash-managing logistics while maintaining the security of your operations, from front-facing cash handling to secure transportation. By outsourcing your cash management and armored transport needs with us, we can help you improve efficiency while reducing errors and downtime.

ATM and ITM Management

With our ATM/ITM Managed Services we can help you address the many challenges of managing an ATM network.

Service Stability and Reduced Costs

Between physical maintenance, cash flow, and software upgrades, the average maintenance cost for an ATM adds up to $1,500 to $5,000 per month, depending on the quality, locations, and other factors. Because we specialize in ATM and ITM services, we offer cost consistencies and improved efficiencies.

Less Downtime

An ATM outage results in angry customers and a loss in revenue. ATM Depot reports that just a few hours of downtime can add up to thousands of dollars in lost transactions, as a loss of reputation and lower confidence in your institution.

Improved Security and Reliability

We use proactive monitoring and maintenance to achieve higher ATM reliability and less downtime, which also improves your customer satisfaction and confidence. It also ensures the security of your network.

We Can Improve Your Cash Handling and ATM Services

Here’s what we have to offer:

- Remote security

- Critical and non-critical software patching

- PCI compliance

- Low-cost check imaging

- Remote troubleshooting, diagnostics, and repair

- Remote deployment of marketing screens

- Preventative Maintenance Inspections

Partner with Shields to Reduce Banking Deserts and Maintain Operations

At Shields, we are proud to do our part to keep the American economy thriving by supporting our communities’ banks and credit unions. Contact Shields to learn more about cash management, coin wrapping, cash-in-transit services, or to obtain a quote. For more valuable industry insights, subscribe to our blog.